Conventional Mortgage Loans: Just How They Compare to Various Other Lending Options

Conventional Mortgage Loans: Just How They Compare to Various Other Lending Options

Blog Article

Comprehending the Numerous Kinds Of Home Mortgage Fundings Available for First-Time Homebuyers and Their Special Benefits

Browsing the array of home loan options offered to new property buyers is crucial for making educated economic choices. Each kind of car loan, from standard to FHA, VA, and USDA, offers distinct benefits customized to varied buyer requirements and conditions. Additionally, unique programs exist to improve cost and supply vital resources for those going into the real estate market for the very first time. Comprehending these differences can dramatically impact your home-buying journey, yet many remain uninformed of the better information that can influence their selections. When examining these alternatives?, what crucial factors should you consider.

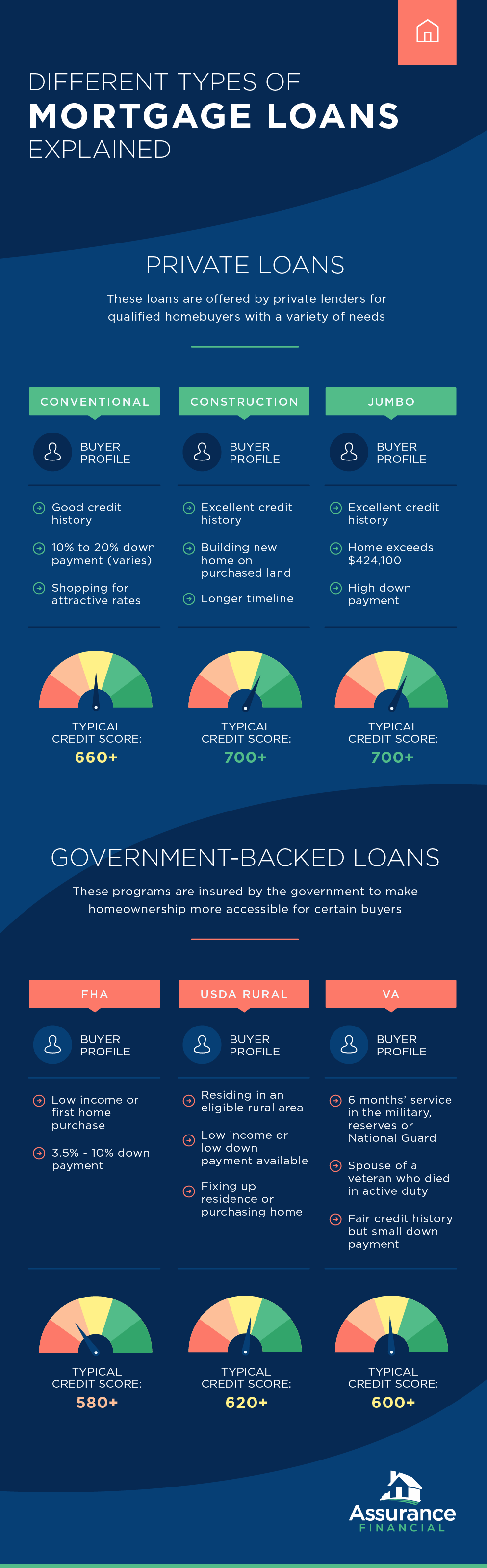

Standard Lendings

Conventional loans are a cornerstone of home mortgage financing for newbie homebuyers, supplying a dependable choice for those looking to buy a home. These loans are not guaranteed or guaranteed by the federal government, which distinguishes them from government-backed financings. Usually, standard car loans need a greater credit scores rating and a more significant down payment, typically varying from 3% to 20% of the acquisition price, depending on the loan provider's needs.

Among the significant advantages of traditional financings is their flexibility. Customers can pick from numerous loan terms-- most typically 15 or thirty years-- enabling them to align their home mortgage with their economic objectives. In addition, conventional lendings may use lower rates of interest contrasted to FHA or VA finances, specifically for consumers with solid credit report accounts.

One more benefit is the absence of upfront mortgage insurance coverage premiums, which are typical with federal government loans. Personal mortgage insurance (PMI) might be needed if the down payment is much less than 20%, yet it can be eliminated once the consumer attains 20% equity in the home. On the whole, traditional car loans present a appealing and viable funding choice for first-time homebuyers looking for to browse the mortgage landscape.

FHA Lendings

For several novice buyers, FHA lendings stand for an available path to homeownership. Insured by the Federal Real Estate Management, these car loans give flexible credentials criteria, making them excellent for those with restricted credit rating or lower earnings degrees. One of the standout attributes of FHA lendings is their reduced deposit requirement, which can be as low as 3.5% of the purchase cost. This considerably reduces the financial obstacle to entry for numerous aspiring home owners.

Furthermore, FHA financings enable for higher debt-to-income ratios compared to standard loans, accommodating debtors that might have existing economic obligations. The rate of interest connected with FHA finances are usually competitive, further enhancing cost. Debtors likewise gain from the capability to consist of specific closing expenses in the financing, which can reduce the upfront economic worry.

Nonetheless, it is essential to note that FHA lendings require mortgage insurance costs, which can raise month-to-month settlements. In spite of this, the general benefits of FHA finances, consisting of availability and lower initial prices, make them an engaging choice for novice homebuyers looking for to get in the realty market. Comprehending these fundings is vital in making informed choices concerning home financing.

VA Loans

VA lendings offer an one-of-a-kind funding service for qualified veterans, active-duty solution members, and specific members of the National Guard and Gets. These best site finances, backed by the U.S - Conventional mortgage loans. Department of Veterans Matters, offer numerous benefits that make own a home a lot more available for those who have actually served the nation

Among the most substantial benefits of useful source VA lendings is the lack of a down repayment requirement, permitting qualified debtors to finance 100% of their home's acquisition rate. This function is specifically helpful for first-time property buyers who might struggle to save for a significant down repayment. In addition, VA fundings typically include affordable interest prices, which can lead to reduce regular monthly payments over the life of the lending.

One more remarkable advantage is the lack of exclusive mortgage insurance coverage (PMI), which is commonly required on conventional finances with reduced down payments. This exemption can cause substantial cost savings, making homeownership a lot more budget friendly. Furthermore, VA finances supply flexible credit rating demands, making it possible for consumers with reduced credit rating to qualify more quickly.

USDA Loans

Exploring funding alternatives, new buyers might locate USDA financings to be an engaging option, particularly for those wanting to buy home in rural or suv areas. The USA Department of Farming (USDA) uses these fundings to promote homeownership in assigned rural areas, offering an exceptional possibility for eligible purchasers.

One of the standout features of USDA fundings is that they require no down payment, making it much easier for newbie customers to go into the housing market. Additionally, these loans usually have affordable rates of interest, which can lead to decrease regular monthly settlements contrasted to traditional funding options.

USDA car loans also include adaptable credit history requirements, enabling those with less-than-perfect debt to certify. The program's revenue restrictions make certain that aid is routed towards reduced to moderate-income family members, additionally supporting homeownership goals in rural neighborhoods.

Moreover, USDA finances are backed by the federal government, which decreases the risk for lenders and can enhance the authorization process for debtors (Conventional mortgage loans). Therefore, novice homebuyers considering a USDA lending may discover it to be a advantageous and available alternative for achieving their homeownership desires

Special Programs for First-Time Purchasers

Several first-time property buyers can gain from unique programs created to aid them in navigating the complexities of purchasing their first home. These programs typically give economic motivations, education and learning, and sources tailored to the special requirements of newbie buyers.

Furthermore, the HomeReady and Home Feasible programs by Fannie Mae and Freddie Mac satisfy low to moderate-income customers, using flexible mortgage options with decreased home loan insurance prices.

Educational workshops held by numerous companies can likewise help newbie purchasers comprehend the home-buying process, improving their chances of success. These programs not only reduce economic concerns yet likewise equip purchasers with knowledge, ultimately assisting in a smoother transition into homeownership. By exploring these special programs, newbie buyers can discover valuable resources that make the imagine possessing a home extra achievable.

Verdict

Conventional lendings are a cornerstone of home loan financing for first-time property buyers, giving a trustworthy choice for those looking to acquire a home. These lendings are not insured or guaranteed by the federal government, which differentiates them from government-backed financings. In addition, traditional lendings might use reduced rate of interest rates contrasted to FHA or VA lendings, particularly for borrowers with strong credit report profiles.

Additionally, FHA finances permit for greater debt-to-income proportions contrasted to standard fundings, accommodating consumers who may have existing financial responsibilities. In addition, VA lendings usually come with competitive interest rates, which can lead to decrease regular monthly repayments over the life of the financing.

Report this page